In the Philippines, there’s a common saying that we are all just “one hospital bill away from poverty.” While it sounds like a dramatic movie line, for many Filipino families, it is a sobering financial reality.

As of 2026, the cost of healthcare continues to rise. Estimates say that in 2026, the cost of treatment for cancer ranges from ₱120,000 to over ₱2,000,000 depending on the cancer type and whether you choose public or private care.

To truly protect yourself and your family, you need more than just “luck”.

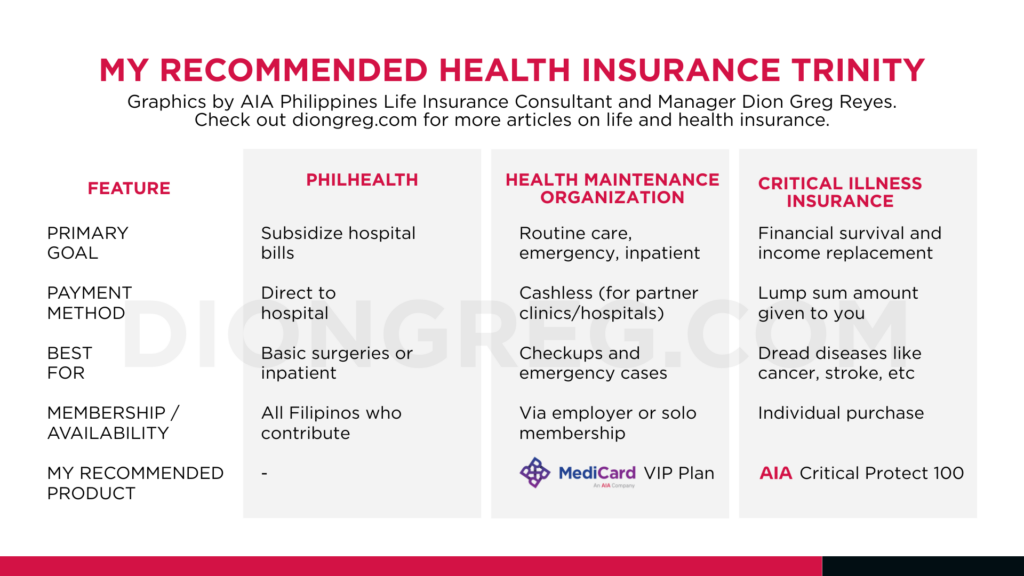

You need to prepare for what lies ahead. This preparation, if you ask me, usually comes in three tiers of ‘health insurance’: PhilHealth, HMOs, and Critical Illness Insurance.

PhilHealth: Support from the Government

PhilHeallth is the mandatory, government-mandated health coverage designed to ensure that every Filipino has access to basic medical services. This is where your taxes go for public healthcare.

While others see PhilHealth is no longer valuable due to the benefits they provide versus the premiums being paid, there is still some worth into it since most hospitals still require PhilHealth contributions as part of the final billing and usually is the first deduction.

If the patient is not a PhilHealth member, the supposed PhilHealth portion is still being charged and becomes an out-of-pocket expense.

Some silver lining: With the restored ₱129.8 billion budget for 2026, PhilHealth has expanded its benefit packages significantly. Coverage now includes higher rates for common conditions like pneumonia and C-sections, as well as specialized “Z-Benefits” for heart surgery and physical rehabilitation.

HMO (Health Maintenance Organization): Privatized Health Benefits

On top of PhilHealth, HMO is your best partner in healthcare. HMOs or Health Maintenance Organizations are private providers (like Maxicare, MediCard, or Intellicare) which has its own network of clinics and hospitals on top of partnerships with private health facilities nationwide.

HMOs are widely used to minimize or zero out costs for prevention, control, and treatment of most illnesses. Transactions under an HMO membership include checkups, diagnostic exams, outpatient, emergency, dental, hospitalization, and annual physical exams, among others. It is mostly cashless which makes the process convenient.

Most Filipinos become HMO members as a company benefit for its employees wherein businesses share risk under a group HMO plan. For those self-employed, they usually avail individual HMO plans.

It’s nice to have both PhilHealth and HMO, but HMO coverages usually have certain limits (Annual Benefit Limit or Maximum Benefit Limit) typically ranging from ₱100,000 to ₱300,000. Given the current medical inflation, this is just not enough and could be easily wiped out after something truly serious happens.

Critical Illness Insurance: Lump Sum for Your Health Expenses

Most people stop at PhilHealth and HMOs, so this is probably one that not many Filipinos get: critical illness (CI) insurance. Unlike PhilHealth or HMOs, which pay the hospital, CI insurance pays you directly in cash upon diagnosis of certain illnesses.

The primary purpose of CI insurance to supplement your PhilHealth and HMO coverage. Treating a major illness like cancer can soar up to P 2.7 million, and it helps to have a CI insurance to cover expenses related to the diagnosis and treatment of this type of dreaded diseases.

Additionally, CI insurance may be thought of as an income replacement if you are unable to work while recovering. Your day-to-day expenses like food and rent are taken care of with a lump sum amount from the CI insurance, usually at least P 1 million.

Not CI insurance plans, however, are the same. Some plans may cover diagnosis of certain illnesses, while others, do not. Make sure to get the most comprehensive one that does not necessarily break the bank.

My Recommended Health Insurance Trinity for Filipinos

Here is a summary of my recommended health insurance trinity for Filipinos:

It pays to prepare for whatever happens in our lives, like getting critically ill. If it is your lived reality today that you are just one hospital bill away from reality, it’s best to talk to an insurance consultant to know more about your options.

Disclaimer: This article/content is AI-assisted for clarity and coherence.