Securing life insurance in the Philippines has evolved significantly. While it used to involve stacks of paperwork and multiple face-to-face meetings, the process in 2026 is a blend of high-tech digital convenience and personalized financial coaching.

Whether you’re a fresh grad, a new parent, or an OFW looking to secure your family’s future, here is your definitive step-by-step guide.

Step 1: Conduct a Financial “Health Check” or Assessment

Life insurance agents or consultants, whether from the agencies or sitting inside banks who underwent proper training always go for a conversation first about an assessment of current financial reality, not pushing a certain product.

Since life insurance is just a portion of personal finance, it is best to conduct a meeting or call with the agent who will make an assessment on the financial situation and where life insurance fits the entire picture.

Here are the typical questions being asked at this stage, among others:

- What is the life insurance for? What is its purpose?

- At what life stage are you currently in?

- Do you have dependents?

- Are savings and emergency funds already in place?

- How much life insurance do you need?

- How much can you set aside for your life insurance premiums?

Step 2: Choose Your Preferred Life Insurance Type

In the Philippine market, most plans fall into these three categories: traditional term, traditional whole life, and variable universal life.

Each type of life insurance serves a specific purpose and has its own features, advantages, and benefits. It is up for you to decide with the guidance of your agent which one to choose or a combination of two or all. Read more about the different types of life insurance plans here. https://diongreg.com/traditional-vs-vul/

Moreover, life insurance plans now include living benefits – meaning you may also include in your life insurance plan some coverage while you are still alive. Called insurance riders, they usually cover risks including accidents, illnesses, and hospitalization.

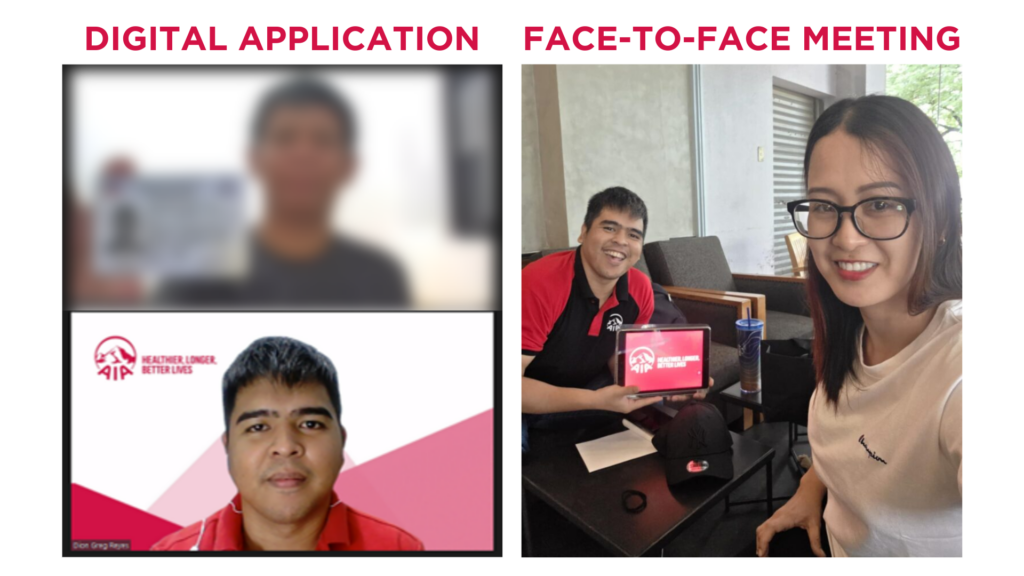

Step 3: Select Your Channel (Digital vs. Traditional)

Among the current life insurance plans available in the market, you have an option to buy through an agent or directly through a website or app. Majority of the companies prefer that you have an agent to guide and assist you along the way from onboarding to claims.

If you have chosen the route to have an agent, you have two ways to be insured once you have chosen a certain life insurance plan:

- Virtually or Digitally. Regulatory body Insurance Commission has allowed the digital selling of life insurance plans during the pandemic, at a time when face-to-face appointments or meetings were limited. Many if not all life insurance companies already allow this type of setup for the purchase, subject to requirements from the agent and client side. And yes, signatures are also done online!

- Face-to-Face. There is still an option for clients and agents to meet face-to-face and onboard the clients. However, purchase is already usually done via a screen – through mobile, tablet, or laptop, with no need for pen and paper to sign.

Step 4: Prepare the Requirements

To keep the process smooth and have an immediate approval of your life insurance application, have these ready:

- Valid Government ID: (e.g., Passport, UMID, Driver’s License).

- Medical Records: If you have pre-existing conditions (diabetes, hypertension), prepare your recent lab results or doctor’s statements.

These documents will be attached to your life insurance application.

Step 5: Complete the Application & Payment

Once you’ve chosen a plan, you will fill out and submit an application form. It usually asks you your contact details, list of beneficiaries, general & lifestyle information, and medical information, among others.

In this regard, always practice full disclosure in each question being asked. If you’re a smoker or have a health condition, declare it. Non-disclosure is the main reason claims get denied in the Philippines.

During the evaluation process or what we call as underwriting, the company will review your “risk” according to your declared occupational and medical conditions. Depending on your age and the amount of coverage, a medical exam might be required.

A life insurance application may only be evaluated upon payment of the applied premiums. Companies now accept different types of payment channels including debit card, credit card, over-the-counter, and online bills payment.

Step 6: The Policy is Issued

Once underwriting is complete and the company agrees to your life insurance application, you will get the approval. Once approved, you will have an effective date and receive your policy contract.

By law, a 15-day “free-look period” from the day you receive your policy serves as protection to you as the client in case you change your mind. In other words, if you realize the plan isn’t right for you upon reviewing the contract documents, you can cancel it and get a full refund of your premium.

And that’s it! Once you complete this process, congratulations! You are now insured.

Talk to a trusted life insurance consultant and experience the onboarding process for your first life insurance plan. Look no further, Dion Greg Reyes is here!

Set an appointment or send an email here: diongreg-b.reyes@aia.com.ph

Disclaimer: This article/content is AI-assisted for clarity and coherence.